The Economics Behind: Building Your Own Private Debt Franchise

In a recent article published by a national newspaper, I came across the headline: “Trump 2.0: More money may venture into Indian Startups.” It struck me as somewhat speculative to assume that the outcome of the U.S. presidential election would directly trigger a surge in the Indian startup equity and debt markets. The article proposed several justifications for this outlook: a possible reduction in corporate taxation for U.S. firms, the possibility of a new era of lower interest rates, the possible redirection of funds from the Chinese tech ecosystem to India’s early-stage startup space due to anticipated trade sanctions by Trump, and the potential support from J.D. Vance, Trump’s Vice President-elect, whose prior career as a venture capitalist might favor such investments.

Notably, the operative word in all these projections is “possible.”

While it is conceivable that the Indian startup ecosystem might experience a resurgence from the prolonged funding slowdown we currently face, the question for entrepreneurs is this: would you prefer to stake your business on possibilities, or would you rather secure its growth with the certainty of capital?

If your answer is the latter, then complementing your equity funding with a strategic allocation of debt becomes imperative. In previous articles, I have addressed the importance of incorporating debt, its primary use cases, and the optimal capital structure founders should leverage to achieve their ambitious goals. This article, however, will shift focus toward the opportunity to establish a private debt franchise for your company—an approach that offers certainty—rather than relying on a speculative shift in the funding environment or the advent of an era of low interest rates.

What is a Private Debt Franchise?

Consider the following scenario: You are the founder of a Series A startup, Company X, which specializes in manufacturing robots and leasing them to customers. The company is currently generating recurring revenue; however, it faces a significant challenge due to a mismatch in cash flows. While there are substantial cash outflows for capital expenditure (capex) required to manufacture the robots, the leasing income is realized incrementally over the tenure of multi-year contracts. This mismatch has resulted in a working capital gap of two months, amounting to INR 5 crore.

To address this gap, Company X initially approached traditional financial institutions to secure a Working Capital Demand Loan (WCDL) facility. However, due to the company’s limited operational history and lack of substantial revenue, lenders required a 100% Fixed Deposit (FD) as collateral. Given the current equity funding crunch, Company X was unable to allocate funds for an FD, making this option unfeasible.

Subsequently, the company explored alternative credit solutions such as venture debt, revenue-based financing, sale-and-leaseback arrangements, and other financing instruments. Unfortunately, these options posed their own challenges, including restrictions related to company vintage, high cost of capital, or the imposition of equity warrants, none of which aligned with Company X's requirements.

Facing these hurdles, Company X appeared to have exhausted its options for raising suitable debt capital.

However, one avenue remained unexplored: Private Debt Issuances, specifically in the form of Commercial Paper (CP) or Non-Convertible Debentures (NCD).

What are CPs and NCDs?

Commercial Papers (CPs) are unsecured, short-term financial instruments with a maturity period of less than one year, issued by a company or a Non-Banking Financial Company (NBFC). The issuance and maintenance of a Commercial Paper require a credit rating. Early-stage startups generally face challenges in obtaining an investment-grade credit rating due to factors such as limited operational history, negative EBITDA margins, and insufficient equity capitalization.

Non-Convertible Debentures (NCDs) are primarily long-term financial instruments, although they can also be issued for shorter durations. These instruments are typically secured, especially when the ticket size per investor is less than INR 1 crore. In such cases, they are mandatorily backed by a charge on receivables or tangible assets. For NCDs with a tenure exceeding one year, a credit rating is not required for issuance and maintenance. However, short-term NCDs (with a tenure of less than one year) must be rated.

Can your Company Issue a Commercial Paper or a Non-Convertible Debt?

Yes, all companies [including start ups] and NBFCs can issue CPs and NCDs basis the master direction criteria issued by RBI and/or the applicable provisions of the Companies Act. Now these change for CPs and NCDs below a 1 year tenure and NCDs over a year tenure.

The Master directions issued by RBI on the criteria and process to be followed for the issuance of CP and NCDs for less than a year are attached below:

For NCD issuances for a tenure of above 1 year, the Companies Act provides the guardrails for issuance.

Please speak to your company secretarial teams on the detailed criteria and process flows for the issuance of CPs/NCDs.

How can Company X leverage CPs and NCDs?

If you, as a founder, have access to capital within your private networks—be it from family, friends, colleagues, or family offices—you can leverage this trust and credibility to establish a private debt franchise. This enables you to raise capital through Commercial Papers (CPs) or Non-Convertible Debentures (NCDs) to address your working capital requirements effectively.

Based on the specific use case—whether it be working capital, asset-liability mismatch, or other needs (as detailed in my earlier article - The Economics Behind: Integrating debt into the capital mix [Startup Debt Series - Part II])—a company like Company X can secure debt capital without relying on traditional financing channels. For example, Company X can issue short-term CPs or NCDs to cover immediate working capital needs, or opt for a long-term NCD with monthly interest payments but no principal repayments until maturity. This structure ensures that significant monthly cash outflows are avoided, aligning with its working capital requirements.

Here is a practical application for Company X:

Addressing the INR 5 Cr Working Capital Gap

Company X has a working capital gap of two months, amounting to INR 5 crore. Historically, this gap was funded through equity capital, which came at a notional yet significantly high cost.

The founder, Mr. Y, has cultivated a strong network of trusted relationships with friends and family offices. Owing to this credibility, they are willing to lend INR 5 crore to Company X.

Overcoming Credit Rating Challenges

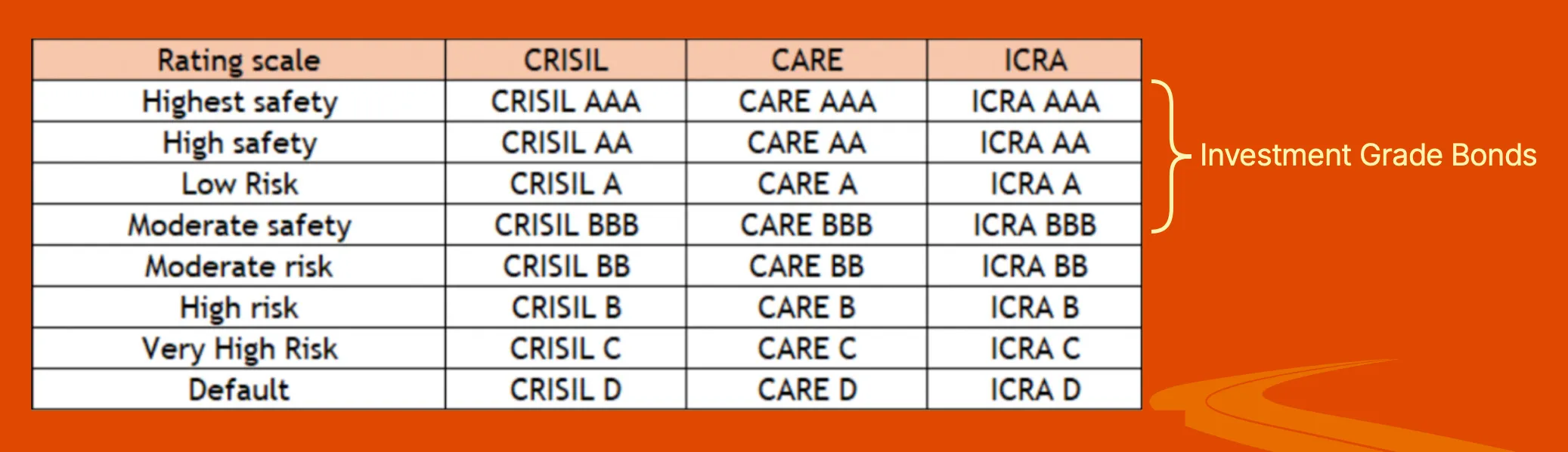

Typically, investors in CPs and NCDs assess the creditworthiness of a company through its credit rating. In India, a BBB rating or equivalent is considered investment grade.

However, given Company X’s limited operational history, low revenue scale, and lack of significant equity on its balance sheet, achieving an investment-grade rating is unlikely. Instead, Mr. Y leverages his personal network to raise the required debt capital on favourable terms, bypassing the stringent conditions imposed by traditional institutions.

As a reminder of the criteria listed earlier - NCDs with a maturity over a year does not require a credit rating. However, CPs and NCDs with a tenure of less than a year neccesitates obtaining a credit rating.

Structure of the Debt Issuance

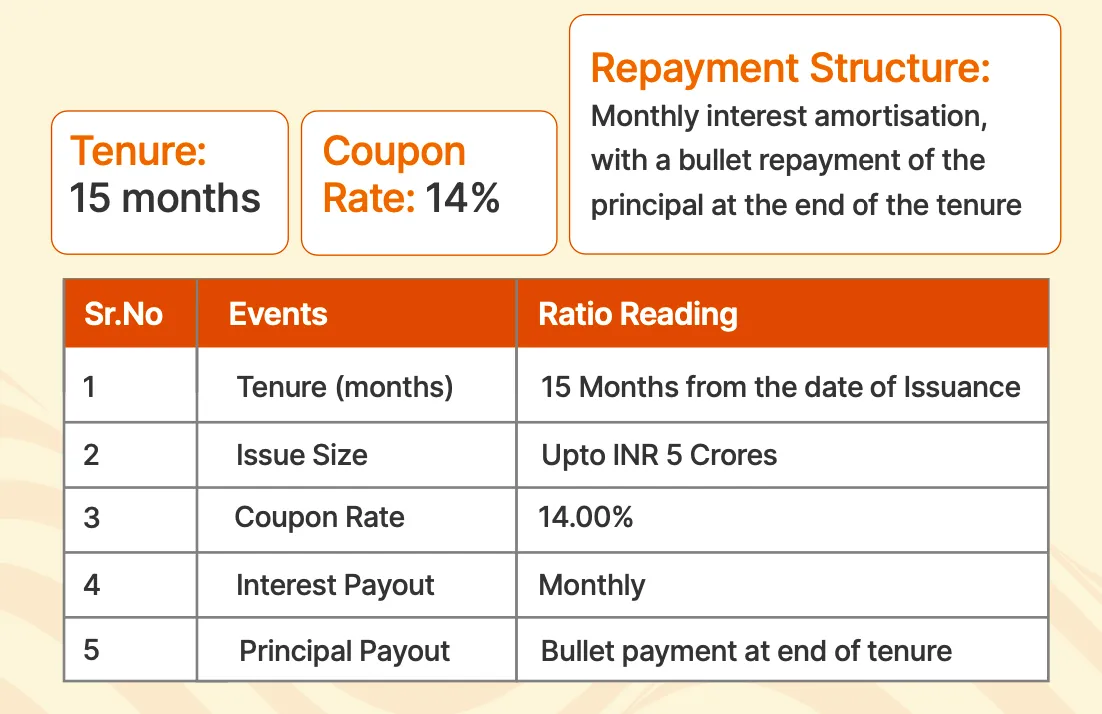

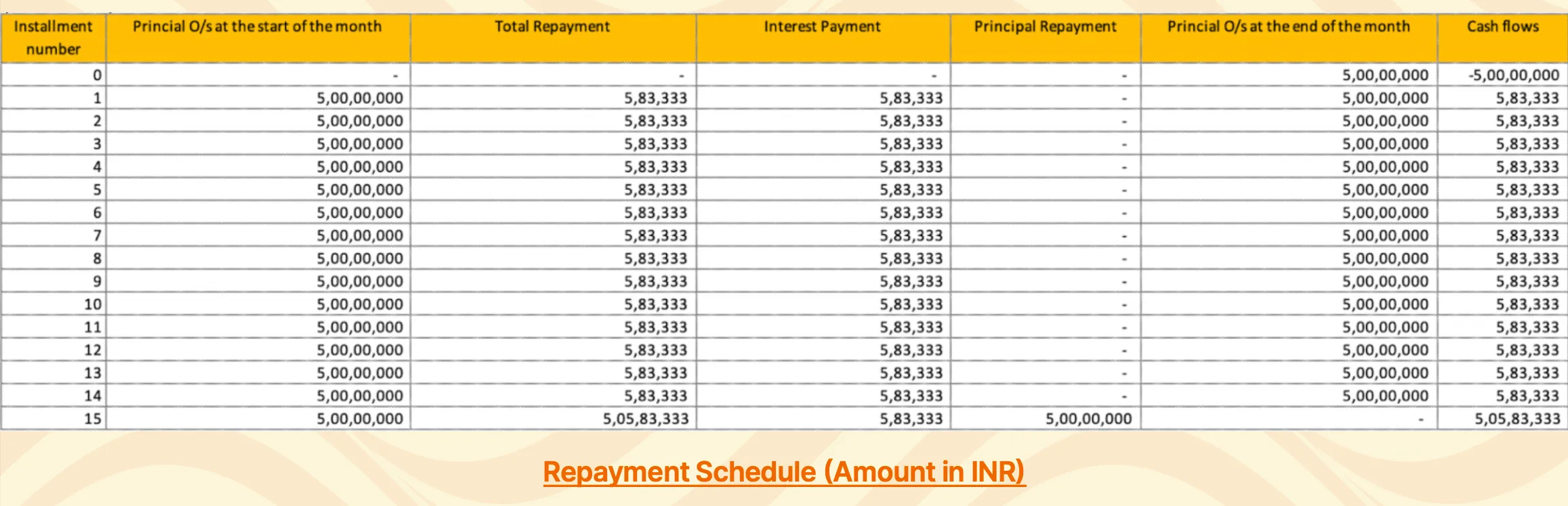

For this transaction, Company X opted to issue an NCD with the following terms:

- Tenure: 15 months

- Coupon rate: 14%

- Repayment Structure: Monthly interest amortisation, with a bullet repayment of the principal at the end of the tenure

This arrangement provided Company X with upfront capital of INR 5 crore to meet its immediate working capital needs, while keeping monthly repayments limited to interest amounts, thereby preserving cash flow. The principal amount of INR 5 crore is to be repaid at the end of the tenure, using:

- Profits generated during the period,

- Additional equity funding secured, and/or

- Further debt issuance through subsequent NCDs.

Outcome

Through this strategic debt issuance, Company X successfully bridged its working capital gap. Moreover, this approach allowed the company to optimize its capital structure, enabling it to focus on growth while maintaining financial flexibility. This serves as a bridge for the company up until it meets the underwriting criteria of traditional and alternative lenders.

Path forward for Company X

A 14% coupon rate may initially appear excessively high and unsustainable at scale, and such a concern would indeed be valid. However, this marks merely the beginning of the journey for Company X. Following this issuance, the company has the opportunity to pursue an investment-grade credit rating from a credible rating agency, aiming for a rating of BBB (or its equivalent).

Below is a snapshot of the credit ratings scale:

To provide context, we analysed BBB-rated issuances available on a leading bond discovery platform. The data highlights yields ranging from as low as 9% to upwards of 15%. The average cost of capital for companies within this rating category, including NBFCs and operationally driven organizations, is observed to be approximately 11-12% p.a. Furthermore, as a company achieves improved credit ratings, the average cost of capital is likely to decrease progressively.

A 3one4 Capital portfolio company, Wint Wealth, is actively working to democratize debt investments for retail participants in India. Collaborating closely with companies and NBFCs that have achieved investment-grade ratings, Wint Wealth facilitates the intricate process of listing Bonds/NCDs on public markets.

Upon achieving investment grade status, Company X can look to leverage not just private sources of capital but also work with companies like Wint Wealth. Wint will enable the company to list its NCDs on public markets and gather public retail investor participation, paving the way for a sustainable approach to raising debt capital.

Conclusion

While debt may traditionally appear as a standardized financial product accessible only through large institutions, this perception is far from accurate. Each debt use case is distinct, requiring equally tailored solutions. This article, along with the preceding parts of this four-part series on startup debt, aims to provide valuable insights for you and your organisation.

If your unique debt problem requires a unique debt solution, please reach out to richard@3one4capital.com

%20(1).jpg)

-p-500.webp)

%20(1).jpg)